A Guide to Inexpensive Health Insurance for Employees and Small Business Owners

An key advantage that guarantees workers may obtain medical care without having to deal with heavy financial burdens is health insurance. Offering health insurance is a crucial tool for small business owners to keep a healthy, productive team as well as an alluring incentive for hiring new employees.

However, small firms with little resources may find it difficult to navigate the complexities of health insurance—understanding pricing, options, and regulatory obligations.

In this article, we’ll explore why health insurance is important for small company owners and employees, the benefits of offering it, and the options accessible to both groups to ensure they have the coverage they need.

Health Insurance’s Significance for Small Business Owners

Offering health insurance may seem like an intimidating and costly obligation for small business owners. Offering health insurance, however, has a number of benefits for both you and your staff.

Draw in and Hold on to Top Talent

One of the perks that employees love the most is good health insurance. Offering health insurance can be a useful strategy to increase your company’s appeal to prospective employees,

as small firms frequently compete with larger corporations for talent. Additionally, it can keep current workers from leaving for companies that provide greater benefits.

Tax Advantages

Owners of small businesses may be eligible for tax credits that lower the price of offering health insurance. The Affordable Care Act (ACA) permits companies with less Increased Productivity and Employee Health

Access to health insurance increases the likelihood that workers will remain healthy, which reduces long-term healthcare expenses, improves productivity, and results in fewer sick days. By making investments in your employees’ health, you contribute to a more reliable and effective workplace.

Employees and Small Business Owners

Adherence to the Law

There may be state-specific requirements, even if the Affordable Care Act does not compel small firms with fewer than 50 full-time employees to offer health insurance. Furthermore, providing health insurance can show your dedication to workers’ welfare, which can increase retention and lower attrition.

Options for Small Business Owners to Get Health Insurance

You have a number of choices as a small business owner when it comes to offering your staff health insurance. The administrative complexity, expense, and coverage of these choices vary.

SHOP, or the Small Business Health Options Program Small businesses can buy for health insurance for their employees through the buy Marketplace, which was established under the Affordable Care Act.

SHOP allows companies with one to fifty full-time employees to examine different plans and select coverage that meets their needs and budget. The ACA’s 10 essential health benefits, which include preventative care, prescription medication, emergency care, and mental health services, must be covered by SHOP insurance.

Businesses can opt to pay in full or in installments because to SHOP’s flexibility in plan creation.

Plans for Health Reimbursement (HRAs) Employers can pay workers for eligible medical expenses and health insurance premiums through HRAs. The Qualified Small Employer HRA (QSEHRA), which is intended for small companies with less than 50 employees, is one of several forms of HRAs.

Without having to buy a group health plan, the QSEHRA enables companies to give workers a certain amount of money annually for health insurance and medical costs.

Because they allow employees to select their own health insurance plan while still offering the company a fixed cost structure, HRAs are a desirable alternative.

Plans for Group Health Insurance Traditional group health insurance plans, in which the employer chooses the plan, may be preferred by certain small firms.

Plans for Individual Health Insurance Employees may think about signing up for individual health insurance plans through the Health Insurance Marketplace if their small business is unable to provide group insurance or if they would rather shop for their own plans. Employees may be eligible for income-based subsidies under the ACA, which can drastically reduce the cost of premiums.

Exchanges of Private Health Another way for small firms to offer health insurance to their staff is through private exchanges. Compared to the government-managed Marketplace, these exchanges, which are run by private insurance companies or brokers, frequently provide a greater selection of plan options.

In terms of how the business organizes its contribution to employee premiums, private exchanges can also provide flexibility.

Employee Health Insurance Important Things to Think AboutPremiums

Employees must pay the monthly fee in order to keep their health insurance coverage. Employees should know how much they will have to spend out of pocket, even though employers frequently contribute to these premiums. It’s crucial to weigh the expenses of premiums against the coverage offered because lower premiums may come with greater deductibles or fewer covered services.

Costs Not Covered by Insurance

Workers should consider additional out-of-pocket costs such coinsurance, deductibles, and copays. Employees may wind up paying more in the long term if a plan with a large deductible has a lower premium, even if it may seem appealing at first.

Provider Network

Typically, health insurance plans have arrangements with a network of physicians, hospitals, and clinics. Prior to selecting a plan, staff members should make sure their Benefits and Coverage

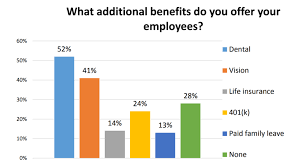

To make sure the plan suits their needs, employees should check its coverage. Essential health benefits are usually covered by health insurance policies, but some may also cover extra services like dentistry, eye, or mental health.

Coverage for Prescription Drugs

Coverage for prescription drugs is frequently a crucial factor, especially for workers who use medication on a daily basis. Workers should confirm that the plan provides inexpensive coverage for their particular prescriptions.

In conclusion

For both employees and small business owners, health insurance is an essential perk. Offering health insurance to employees can benefit firms by attracting and keeping talent, enhancing worker productivity and health, and possibly offering tax benefits. Health insurance helps employees maintain their general well-being, lowers financial risk, and gives them access to necessary care.

The SHOP Marketplace, HRAs, and group or individual plans are just a few of the health insurance alternatives that small company owners should be aware of. You can discover a solution that provides useful coverage without going over budget by carefully weighing your needs and those of your staff.